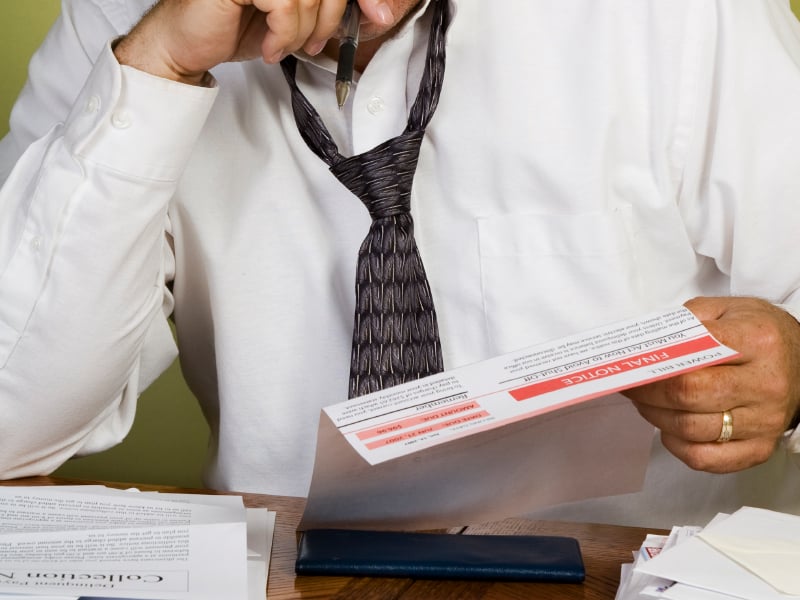

Here’s the first thing you should know about debt collection: The people calling you every day aren’t the people you borrowed from years ago. You’re likely speaking with someone from a collection agency. And if your debt is several years old, there’s a good chance that the collector on the line may not play by the rules.

In 2013, federal agencies received more than 200,000 consumer complaints, the U.S. Consumer Financial Protection Bureau reported last year. While larger collections companies may follow regulations more closely, smaller operations can fly under the radar more easily. Recordkeeping is minimal, and information about debts and interest is sold multiple times and sometimes stolen.

“You’re talking to someone who’s bought your debt for pennies on the dollar,” says Jake Halpern, author of “Bad Paper: Chasing Debt from Wall Street to the Underworld.” “They’re trying to make a tidy profit from it.” One old-debt specialist Halpern profiled has served prison time for armed robbery, and several other collectors he writes about also have criminal records or drug problems.

Whether you’re dealing with a corporate firm or a hole-in-the-wall collections shop, it’s easy to feel overwhelmed. But having an overdue bill go into collections isn’t — and shouldn’t be — a life sentence. Before negotiating with a collector, here’s what you should know:

1. Sometimes you can’t be sued.

If your debt is older than your state’s statute of limitations, you’re beyond the reach of lawsuits. After seven years, accounts that have gone into collections won’t show up on your credit report, either. But in terms of your credit score, if your debt is that old or older, paying it likely won’t help you. In some cases, paying the debt may even revive it on credit bureau reports and it may show up for another seven years, which could hurt you.

Strategy: Ask the collector if the debt is time-barred. Because of the Fair Debt Collection Practices Act, collectors have to answer that question truthfully. If they don’t answer, write a letter disputing the debt and requesting verification within 30 days of receiving the call. Wait until you get verification before deciding whether to pay.

2. Your debt may have been sold or stolen.

Ramon Khan, 28, who worked for a major debt collection company starting at age 16 in Houston, says that selling debt multiple times or stolen information are a common problem for debt collectors, even among the more corporate variety.

“It was very normal to hear things like, ‘We keep paying for it, but it doesn’t go away,’” Khan said by phone. This makes it easy for consumers to overpay the debt without getting their credit reports updated.

Strategy: Do your research and keep good records.

“You want to make sure you’re paying the person who actually owns the debt,” says Halpern. That means requesting debt verification early on and checking out the company with the Better Business Bureau or the federal consumer agency to make sure the collector is reputable.

Once know you’re corresponding with the right company, conduct all related transactions by mail and make copies of everything. Create as much of a paper trail as possible, so that if anything doesn’t go as discussed, disputing the transaction is easier.

3. Your credit report won’t be squeaky clean after you pay.

Collections appear on credit reports for seven years. But they may be listed as “paid in full” if you handed over what was owed and the records were updated.

If a negotiated settlement lowers what you pay, it could get more complicated, says Khan, who quit the collections business a decade ago. In many cases, “it gets put on your credit report as a partial settlement,” he explains. Typically, he says, the remaining balance is sold to another debt buyer and the debtor would still receive calls about it. For someone who thought they had paid off their debt, this may be a rude awakening.

Strategy: Before paying, make sure the account is reported as “paid in full” to credit bureaus. Get a written statement from the collection company to this effect before you pay and check your credit report for the change afterward. Once the debt is marked “paid in full,” creditors may look at it more favorably.

4. If a collector breaks the rules, you can report it.

After five of her credit cards went into collections some years ago, Deborah Glassman, of Mar Vista, California, remembers getting calls as early as 7:30 a.m. and as late as 10:30 p.m. Her commercial printing business had slumped and the Great Recession made recovery difficult.

“There was one guy who was really yelling and screaming at me,” Glassman recalls in an interview. “He said, ‘I’m going to find you.’ That was unnerving. He was like one of those hit men in the movies.”

Glassman stopped taking calls from that number and believes the account was sold to another collections company. She agreed to settlements on three of her credit card accounts and avoided bankruptcy, but the experience left her shaken.

Strategy: Document collector law-breaking by writing down what happened and when. Remember, debt collectors aren’t allowed to threaten you, use profanity or call you repeatedly. A collector can’t falsely claim to be a police officer or a lawyer. If you report these violations to the CFPB or the Federal Trade Commission, the company may face large fines. You also have the option to sue for damages.

5. Being sued for debt doesn’t mean you’ll lose.

Don’t skip a court hearing just because a collector sues. If you don’t show up, the judge may hold you in default.

Strategy: Go before the judge. Avoid settling out of court. In “Bad Paper,” Halpern describes a scene where a lawyer pressures a couple to sign a paper acknowledging a purported debt before trial. The paper looks like a credit card bill, but it isn’t. The couple won’t sign and the lawyer subsequently withdraws the complaint against them.

Don’t be misled or intimidated by collection tactics like these, Halpern says. A lawyer may be able to help you countersue for damages, he says. But if you can’t afford a lawyer, make sure you keep asking for verification of the debts in collection.

“If someone says, ‘Is this your debt?’ say, ‘I can’t be certain that this is my debt unless I see more accurate and detailed information, like account statements and original signed contracts,’” he says. “‘Until I see that, I have doubts.’”

Move on

Constantly getting phone calls reminding you of your past failures can be haunting. But Glassman, who recently started a new business selling prepackaged cocktails, tells other people who are dealing with debt to treat it like you would any transaction. Communicate with your creditors, she says, and once you’ve resolved the issue, keep looking forward.

“You don’t want debt to define you,” she says. “You want to get past it.”